作者:magicdhz

This post is part of our special coverage Egypt Protests 2011.

翻譯:白話區塊鏈

Translation: White section chain

主要要點:

Main points:

由Lido DAO管理,Lido協議是一個開源中間件,用於將ETH、stETH和以太坊的獎勵傳輸到一組驗證者和ETH質押者之間。

Managed by Lido DAO, the Lido agreement is an open-source intermediate for transferring ETH, stethH and Ether's awards to a group of testers and ETH detainees.

stETH是最流動的LST,並且是最廣泛使用的鏈上抵押品形式。

StETH is the most fluid LST and the most widely used chain-based form of collateral.

stETH的流動性和stETH作為抵押品也在中心化交易平台上成長,顯示機構傾向於透過交易和持有stETH來取代ETH。

The fluidity of steth and stethh as collateral have also grown on a central trading platform, showing the institutional tendency to replace ETH by trading and holding steth.

透過強大的驗證者組合質押,stETH的風險較低,並提供更高的機率調整回報。

Through a combination of powerful witnesses, the risk of stETH is lower and offers a higher chance of adjusting.

由於傳統金融尋求質押ETH獎勵,這可能意味著開發"傳統金融ETH"產品,stETH作為協調工具可以抵制中心化趨勢。

As traditional finance seeks to secure ETH rewards, this may mean development & quot; traditional ETH& quot; and products, stETH as an instrument of coordination to counter centralization.

2024年5月20日,Eric Balchunas和James Seyffart將現貨ETH ETF核准的幾率從25%上調至75%。 ETH在幾個小時內上漲了約20%。然而,根據美國證券交易委員會(SEC)的要求,發行人修改了S-1註冊聲明,將質押獎勵從ETF中移除。因此,持有現貨ETH ETF的投資者將無法獲得以太坊的質押獎勵,可能是因為提供質押ETH產品需要必要的監管明確性。無論如何,按照當前利率,選擇持有現貨ETH ETF的投資者將損失約3-4%的年化收益率,這是共識和執行層獎勵所帶來的。因此,為了減少稀釋,有動機將質押納入ETF產品中。

On May 20, 20, 2024, Eric Balchunas and James Seyffart increased the rate of approval of the current ETH ETF from 25% to 75%. The ETH rose by about 20% in a few hours. However, at the request of the United States Securities and Exchange Commission (SEC), the issuer modified the S-1 register to remove the pledge from the ETF. Thus, investors holding the current ETH ETF would not be rewarded by the taupuleta, probably because the necessary oversight would be required to provide the ETH product.

Lido協定是一個開源中間件,根據委託標準自主地將ETH匯集路由到一組驗證者中。由LDO持有人管理的Lido DAO管理前述委託標準的一些參數,如協議費用、節點操作員和安全要求。然而,該協定是非託管的,DAO不能直接控制底層的驗證者。佔網路總質押的約29%(9.3百萬ETH,即358億美元),stETH是質押產業中的重要基礎設施,其效能、委託和其他質押實務要求都處於較高水準。

Lido's agreement is an open-source middle, autonomously and in accordance with the Commission's criteria, to transfer the ETH channel to a group of testers. Lido DAO, managed by the LDO holder, manages some of the parameters that the commission has mandated, such as the cost of the agreement, node operators and security requirements. However, the agreement is uninvited, and the DAO has no direct control over the bottom. About 29% of the total Internet pledge (9.3 million ETHs, or $35.8 billion), the stETH is an important infrastructure in the delivery industry, and its effectiveness, commissions and other security requirements are high.

ETHETF可能是傳統金融投資者今天獲得ETH暴露的最便利選擇,但這些產品無法捕捉到以太坊的發行或加密經濟活動。隨著更多傳統金融場所自行連接Token,持有Lido的流動質押TokenstETH可以說是獲得ETH和以太坊質押獎勵的最佳產品,因為它在現有市場結構中具有以下關鍵用途:

ETHETF may be the most convenient option for traditional financial investors to be exposed to ETH today, but these products cannot capture Ether’s launch or encrypted economic activity. With more traditional financial establishments connecting themselves to Token, TokenstETH’s fluid pledge by Lido can be described as the best product to be rewarded by ETH and Ether, because it has the following key uses in existing market structures:

stETH是去中心化交易平台(DEXes)上流動性最強、交易量最大的ETH質押資產。

StETH is the most dynamic and traded ETH-carried asset on the decentralised trading platform (DEXes).

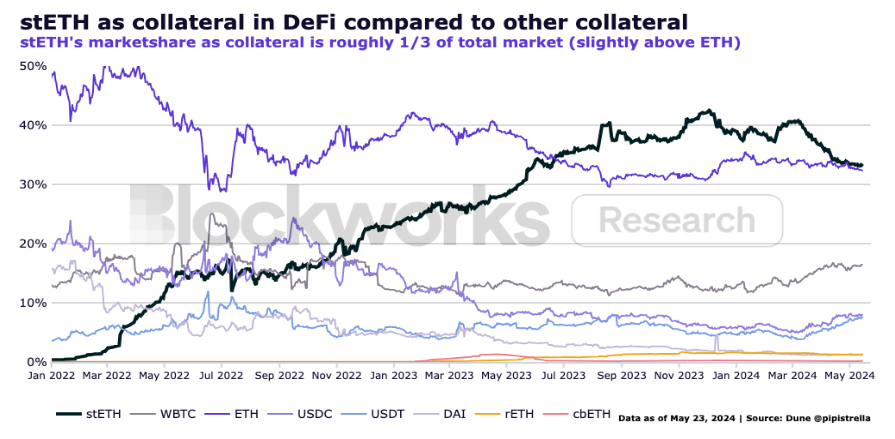

stETH是DeFi中最廣泛採用的抵押品形式,超過了最大的穩定幣USDC和ETH本身。

StETH is the most widely used form of collateral in DeFi, exceeding the largest stable currency USDC and ETH itself.

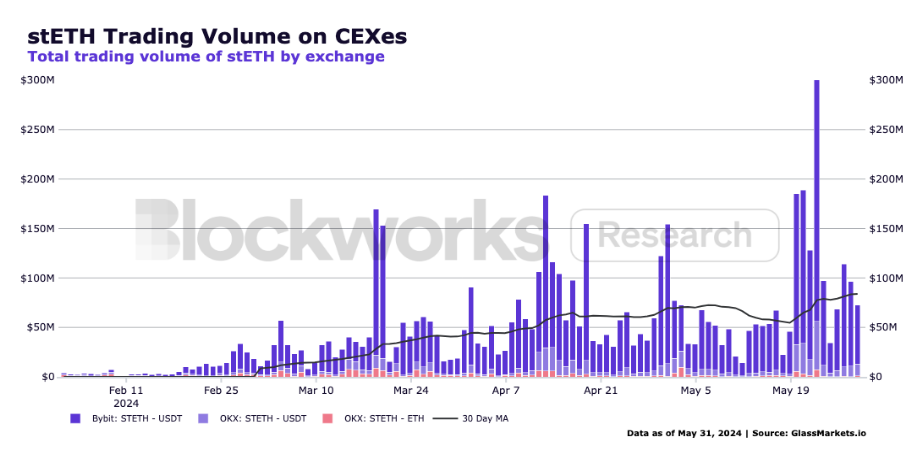

stETH是集中交易平台(CEXes)上最具流動性且具有獎勵的L1原生資產,作為現貨ETH交易的替代品和抵押品形式不斷增長。

StETH is the most dynamic and rewarding L1 primary asset on a centralized trading platform (CEXs) and is growing as a substitute for and collateral for the current ETH trade.

隨著ETH ETF的出現,stETH的主導地位有可能持續存在,因為投資者對以太坊的了解更多,並尋求來自共識和執行層獎勵的額外回報,這對於鞏固更強大的stETH市場結構來說是有利的。更進一步展望,隨著傳統金融機構最終將質押納入其產品(稱為「傳統金融ETH」),Lido DAO的治理和stETH的成長變得至關重要,以維持以太坊上足夠分散的驗證者組合。

With the advent of ETH ETF, the dominant position of stETH is likely to persist, as investors know more about Etheria and seek extra rewards from the consensus and executives, which is beneficial for the stronger market structure of stETH. Looking further, as traditional financial institutions finally commit their products (known as "traditional financial ETH" ), Lido DAO’s governance and growth of stETH become critical to sustaining a sufficiently fragmented portfolio of witnesses in the community.

因此,“stETH > 傳統金融ETH”,因為它提供更好的回報,比相鄰產品擁有更多的實用性,並作為對抗中心化的協調工具。

As a result, “stETH & gt; traditional financial ETH”, which provides better returns, has more practical applications than neighbouring products and is used as an instrument of coordination against centralization.

Lido協議的中間件是一組智慧合約,透過程式化地將使用者的ETH分配給經過審查的以太坊驗證者。這個流動質押協議(LSP)旨在增強以太坊的本地質押能力。它主要為兩個參與者提供服務:節點操作員和ETH質押者,並解決了兩個問題:驗證者的准入門檻和將ETH鎖定以進行質押而導致的流動性損失。

In the middle of the Lido agreement, a group of intellectual compacts distributed the user's ETH to a censored Ethio-based tester. This fluid pledge agreement (LSP) is designed to enhance the local capacity of the community. It serves two participants: node operators and ETH-depositors, and solves two problems: the access door for the tester and the fluid loss caused by locking the ETH to make the pledge.

儘管在以太坊上運行驗證者的硬體要求不像其他鏈那麼高,但為了參與共識,節點操作員需要在驗證者中質押恰好32個ETH的增量以獲得以太坊的獎勵。籌集這麼多資金不僅對於潛在的驗證者來說並不容易,而且在32個ETH的限制下分配ETH可能效率極低。

Despite the fact that the hardware requirements of the tester operating at the Etheria are not as high as those of the other chains, in order to be part of the consensus, node operators need to hold an increase of exactly 32 ETHs among the tester to be rewarded by Ether. It is not only not easy to raise this amount of money for potential tester, but the distribution of ETHs under 32 ETHs may be extremely inefficient.

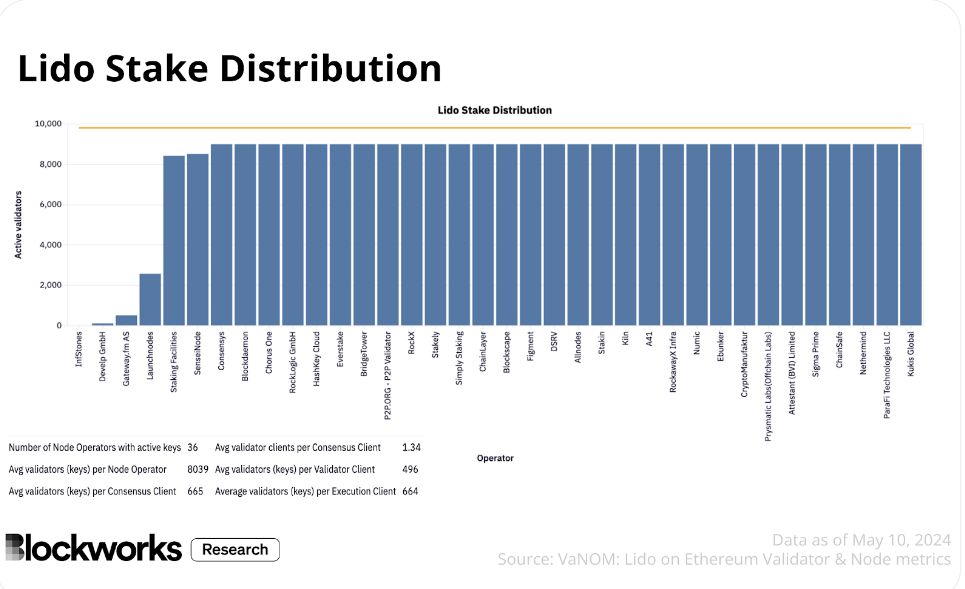

為了簡化這個過程,Lido將來自投資者的ETH路由到驗證者組合,並有效降低了高經濟門檻。此外,透過嚴格的評估、監控和節點操作員間的委託策略,Lido DAO減輕了驗證者組合的風險。可以在此處找到包含來自驗證者組合的操作員統計數據和指標數據。

In order to simplify the process, Lido combines the ETH route from the investor with the tester, which effectively reduces the high-income economy. In addition, Lido DAO mitigates the risk of the tester grouping through a rigorous evaluation, surveillance, and node operator strategy.

作為對他們的ETH存款的回報,投資者會獲得stETH,並且其價值主張很簡單。運行驗證者或質押ETH需要將ETH鎖定在一個帳戶中,而stETH則是一種流動的實用Token,用戶可以在CeFi和DeFi中使用。

In return for their ETH deposits, investors get stETH, and its value is simple. The operator or hostage ETH needs to lock the ETH in an account, while the stETH is a moving user of Token, which can be used in CeFi and DeFi.

1)stETH

stETH是一種流動的質押Token(LST),屬於實用Token的一種,它代表了存入Lido的ETH總額,加上質押獎勵(減去手續費)和驗證者處罰的金額。手續費包括從驗證者、DAO和協議中收取的質押佣金。

STETH is a fluid type of hostage to Token (LST), a form of practical use of Token, which represents the sum of ETH deposited in Lido, plus the amount of money to be fined (reduced) and to be punished by the tester. The fee consists of a pledge commission from the tester, DAO, and the agreement.

當用戶將1個ETH存入Lido時,會發行1個stETHToken,並發給用戶,協議會記錄用戶在協議中所持有的ETH份額。該份額每天進行計算。 stETH是用戶可以兌換為他們在資金池中所持有的ETH份額的憑證。透過持有stETH,用戶可以透過重新基準機制自動獲得以太坊的獎勵,基本上隨著獎勵的累積到驗證者組合,協議會根據帳戶在協議中持有的ETH份額來發行和分發stETHToken。

When the user deposits an ETH in Lido, a stETHToken is issued to the user, and the agreement records the amount of ETH held by the user in the agreement. This amount is calculated every day. The stETH is a certificate that the user can exchange for the ETH amount they hold in the pool. Through the holding of stETH, the user can receive self-initiated ETH awards through the re-establishment of the standard system and basically accumulates to the tester group with the rewards, and the council issues and distributes the stETHToken according to the number of ETHs held by the account in the agreement.

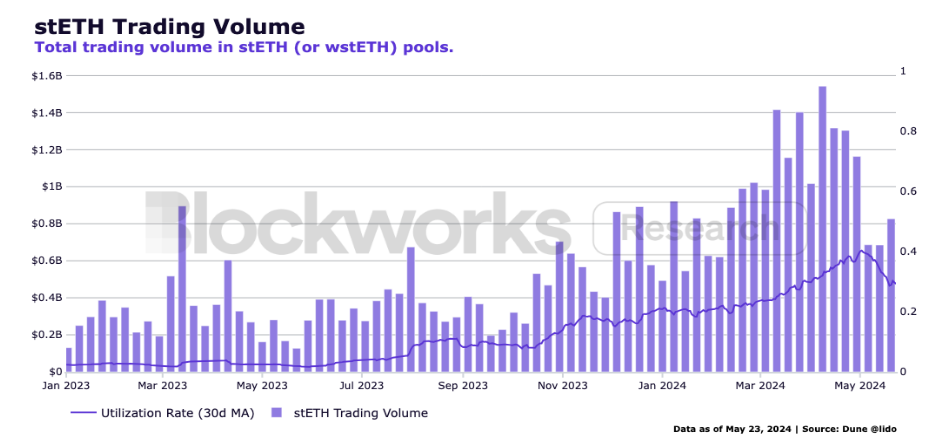

在同一時間段內,stETH的交易量和在這些池中的利用率都有增加。以下圖表中的趨勢顯示:

During the same time period, the volume of transactions at stETH and the utilization rate in these pools have increased.

- 流動性提供者更加穩定和一致

- 市場對於stETH的流動性已經接近更穩定的均衡點

- 越來越多的參與者更習慣於交易stETH

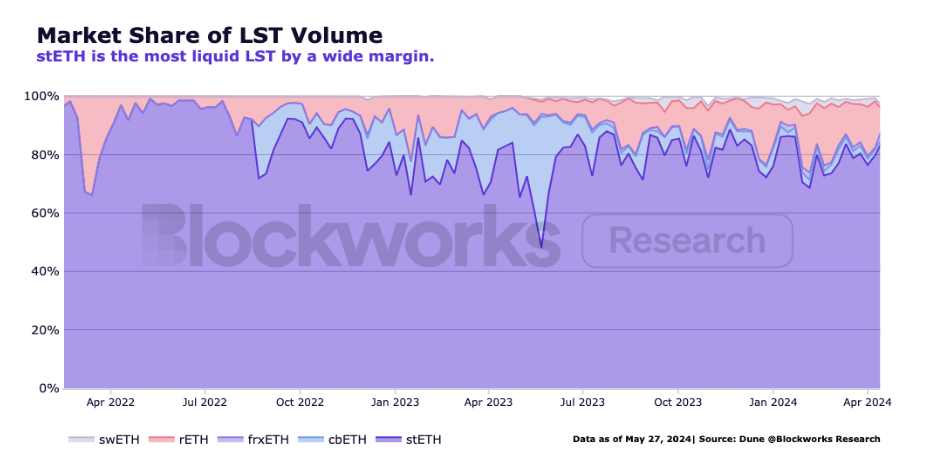

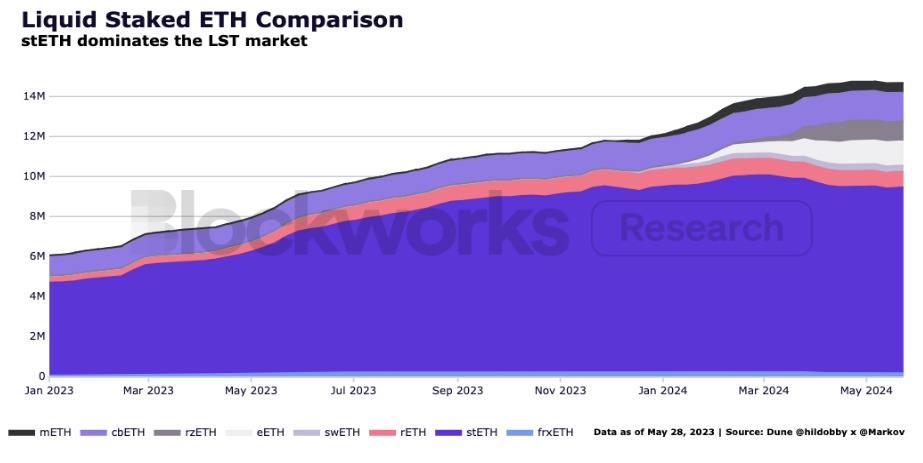

與將LDO激勵費用過度花費在季節性流動性提供者相比,這些市場結構為擴張提供了更強大和有機的基礎。如下圖所示,與其他流動性質押Token(LST)相比,stETH的交易量和流動性佔據明顯的主導地位。

These market structures provide a much stronger and more dynamic basis for expansion than they use the LDO incentive to spend too much on seasonal fluids. As shown in the figure below, the volume of transactions and fluidity in stETH is clearly the main guiding position compared to other fluid-carried Tokens (LSTs).

流動性非常重要,流動性可以說是金融市場風險管理的最大決定因素。資產的流動性狀況對其風險調整報酬率有著很大的影響,進而影響其對投資者的吸引力。這使得stETH對於希望獲得以太坊獎勵的投資者和交易者來說是一個更好的選擇,這在一個由Hashnote、Copper、Deribit和Cumberland等大型加密本地機構參與的Blockworks小組討論中得以證明。下面的圖表顯示了加密本地機構在中心化交易平台上採用stETH的趨勢:越來越多的加密本地機構和市場製造商更傾向於持有和交易stETH。注意:由於交易平台更改了訂單簿資料的速率限制,二月和三月的全球出價資料有部分不完整。

Flowability is very important, and mobility can be described as the biggest determinant of financial market risk management. The liquidity situation has a significant impact on risk adjustment rates and has an impact on the attractiveness of investors. StETH is a better option for investors and traders wishing to get an Ether prize, as evidenced by the discussions in Blockworks, a small group of large encrypted local institutions such as Hashnote, Copper, Deribit, and Cumberland.

4)stETH作為抵押品

stETH也是DeFi中最受歡迎的抵押品,甚至超過了ETH和流行的穩定幣,如USDC、USDT和DAI。下圖顯示,自推出以來,它逐漸攀升至該位置,大約佔據了總市場份額的三分之一左右。

StETH is also the most popular collateral in DeFi, even exceeding ETH and popular stable currencies such as USDC, USDT, and DAI. The figure below shows that, since its launch, it has risen to that position, accounting for about one third of the total market share.

將stETH作為高品質的抵押品選項使其資本效率提高,並可能幫助交易平台和借代平台增加額外的交易量。今年2月,Bybit宣布將stETH的抵押價值從75%提高到90%。自那時以來,Bybit上的stETH交易量增加了近10倍。

Bybit announced in February this year that it would increase the value of its mortgage from 75% to 90%. Since then, the volume of its transactions on Bybit has increased almost tenfold.

看起來stETH在鏈上的市場結構已經達到了一個更穩定的均衡點,這可能為逐漸長期成長趨勢奠定了堅實的基礎。在鏈下,我們可以觀察到更多機構的採用跡象,因為投資者更傾向於選擇質押的ETH而不是普通的ETH。雖然我們也預期其他流動性質押Token(包括可能是流動性質押權證)會獲得市場份額,但是stETH現有的市場結構和主導地位以及先行者優勢應該會保持其在市場上的強勢地位。此外,Lido和stETH相比其他質押選擇具有一些有利的特性。與其他質押機制相比,Lido的機制有三個關鍵特點:非託管、去中心化和透明。

It seems that the market structure of stETH on the chain has reached a more stable equilibrium, which may provide a solid foundation for a long-term progression. Under the chain, we can observe more evidence of the use of institutions, because investors tend to choose the ETH rather than the ordinary ETH. Although we also anticipate that other fluid threats to Token (including possibly mobile security rights) will be marketed, the market structure and guiding position that STETH now has, as well as the vanguard advantage, should maintain its strong position on the market. In addition, Lido and StETH have a number of advantages compared to other pledge options.

非託管:Lido和節點運營商都不會託管用戶的存款。這個特性減輕了交易對手風險,節點業者永遠不會掌握用戶質押的ETH。

No authority: Lido and node operators do not charge the user’s deposits. This feature reduces the risk to the counterparties, and node operators will never have access to the user’s ETH.

去中心化:沒有一個單一的組織對該協議進行驗證,技術風險平均分佈在一組節點運營商之間,提高了彈性、可用性和獎勵。

Decentralizing: No single organization has tested the agreement, and the technology risks are distributed equally among a group of nodes, increasing the resilience, availability and rewards.

開源:任何人都可以審查、審計和/或提出改進建議來運行該協議的程式碼。

Open Source: Anyone can review, screen and/or propose changes to the code of the agreement.

當stETH與其他流動性質押Token(LST)和質押服務提供者進行比較時,根據Rated的數據,按總質押量排名靠前的節點運營商之間的獎勵差異很小,大約在3.3-3.5 %之間。然而,考慮到營運節點的因素,包括維運、雲端基礎設施、硬體、程式碼維護、用戶端類型、地理分佈等,獎勵的微小差異包含了許多風險。

When stETH compares with other fluid delivery providers of Token (LST) and pledge services, according to the Rated data, the difference in reward ratings by aggregate amount to the previous node operator is small, ranging from 3.3 to 3.5%. However, considering the factors at the node, including maintenance, cloud infrastructure, hardware, code maintenance, client type, geographical distribution, among others, there are many risks involved.

stETH的風險較低,因為它確保了對多個運營商的暴露,這些運營商在不同的地點運行不同的機器、代碼和客戶端,並由許多團隊管理。因此,宕機的可能性較低,且風險預設更加分散;而其他質押服務提供者的營運則更加集中,存在潛在的單點故障。關於該領域的更多信息,Blockworks研究分析師0xpibblez撰寫了一份詳盡的研究報告。

The risk is lower because it ensures exposure to a number of operators who operate different machines, codes, and clients at different locations, and are managed by many teams. As a result, the probability of crashing machines is lower and the risks are more diffused; and other providers are more concentrated, with potential single-point failures. For more information on the field, Blockworks Research Analyst 0xpibblez wrote an exhaustive study.

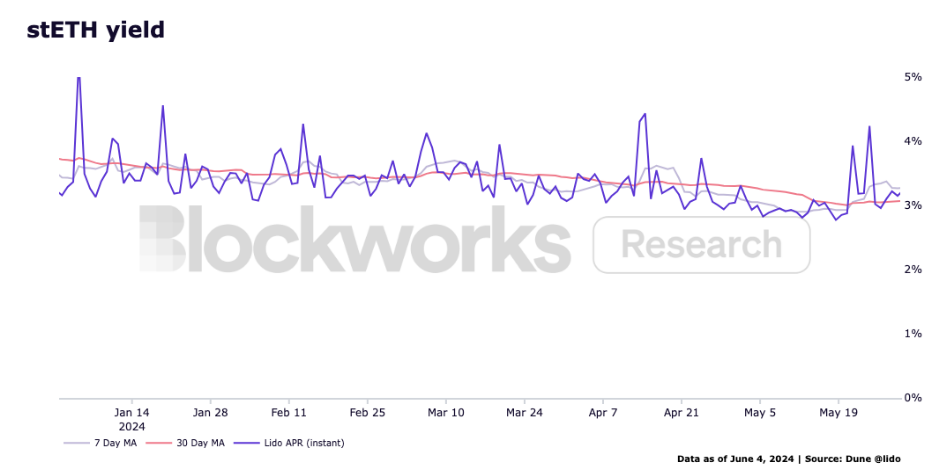

5)stETH超額獎勵的機率

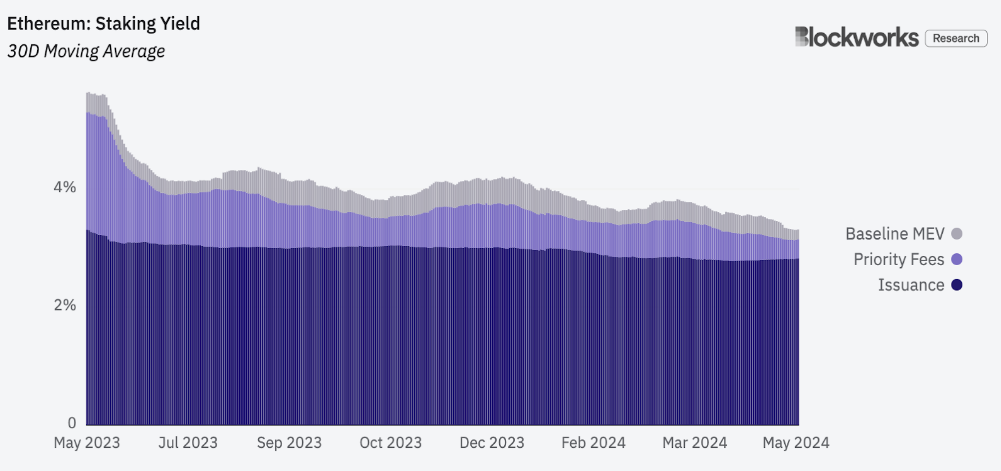

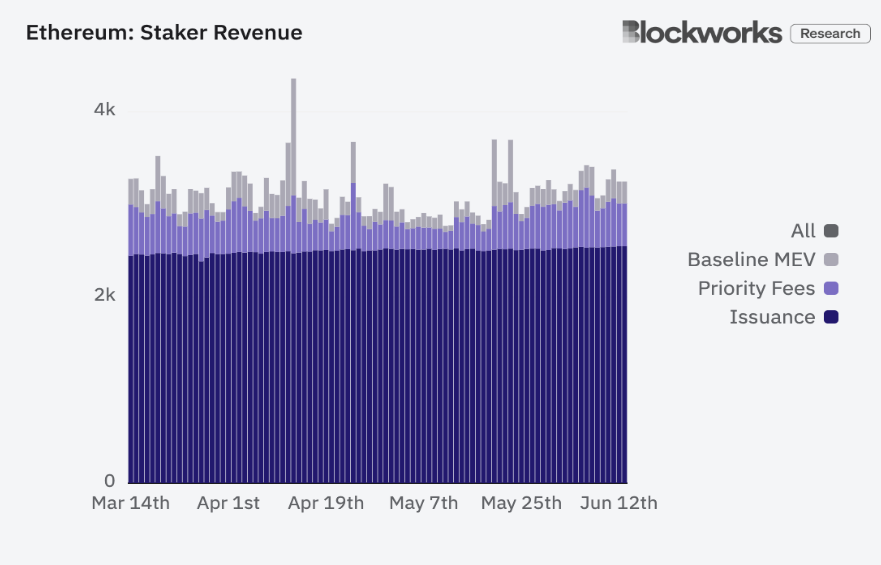

參考下面的第一張圖,我們可以觀察到執行層獎勵(優先費用+基線MEV)比共識層獎勵(發行量)更有變化。下面的第二張圖顯示了過去一個月內這種變化的放大視圖。這是由於鏈上活動的周期性特徵,即在某些時期,活動水平升高與更有價值的區塊和因此更高的執行層獎勵相一致;而共識層獎勵是恆定的。這意味著實現的質押ETH獎勵是驗證節點提議下一個區塊的機率的函數,捕捉了執行層獎勵的變化性。

Looking at the first graph below, we can observe that the executive-level reward (plus base line MEV) is more variable than the corporate-level reward (volume distribution). The second graph below shows the magnifying picture of this change over the past month. This is due to the cyclical nature of the activity on the chain, in which, at some times, the level of activity coincides with the value-added block and the resulting higher enforcement-level reward; and the shared-level reward is permanent. This means that the actual pledge of the ETH reward is the function of verifying the probability of the next block in the programme, capturing the variability of the executive-level incentive.

由於stETH在一個廣泛多樣的運營商中進行質押,並代表了總質押的29%,因此stETH捕捉區塊獎勵的變化性的概率要比獨立驗證節點、較小的運營商或質押量較少的驗證節點集更高。這意味著它平均而言始終能夠獲得更高的獎勵率。

Since StETH is being held hostage in a wide variety of operators and represents 29% of the total, the probability of stETH capturing block rewards is higher than the number of independent test nodes, smaller operators, or less. This means that on average it will always get a higher reward.

換句話說,在極端情況下,當一個獨立驗證節點提議一個極具價值的區塊時,即使總回報率要高得多(例如,質押32個ETH在一個區塊中賺取10個ETH) ,這種情況發生的機率非常低,大約是一百萬分之一(32/32,400,000)。他們基本上贏得了一場彩票。而另一方面,Lido的驗證節點集更有可能捕捉有價值的區塊,大約有29%的時間。因此,持有stETH的用戶選擇並且加強了分享更多獎勵的機會。

In other words, in extreme cases, when a stand-alone test node proposes an extremely valuable block, even if the overall return rate is much higher (e.g., the pledge of 32 ETHs to earn 10 ETHs in one block), the probability is very low, about one million (32/32,400,000). They basically win a lottery. On the other hand, Lido’s test node collection is more likely to capture valuable pieces, about 29% of the time.

總之,stETH作為獲取質押ETH獎勵曝光的優越選擇的另一個原因是它在機率和風險調整的基礎上產生了極具競爭力的獎勵。

In any case, another reason why stETH is a superior choice to be exposed as a hostage-taking ETH prize is because it generates a highly competitive reward on the basis of both probability and risk adjustment.

現貨ETHETF的批准帶來了對額外產品的期望,其中最明顯的一個是質押ETH產品。在他的牛市週期休息期間,加密原生傳奇人物DegenSpartan寫了一篇名為《我們可以推出多少特洛伊木馬? 》的貼文。在這篇簡短的部落格文章中,DegenSpartan寫道:「在現貨ETF之後,我們仍然可以期待在[傳統金融]領域獲得更多的接入,期權,納入基金組合,共同基金,退休賬戶,定投計劃,結構化產品,雙幣種,蘭巴德貸款等等。

In this short blog post, DegenSpartan writes: “After the current ETF, we can still expect more access in the [traditional financial] domain, options, access to funds, mutual funds, retirement accounts, investment plans, construction products, double currency, Rambad loans, etc.

雖然美國的資本市場將更多地接觸到ETH,帶來更多的永久性(結構性)風向,但尚不清楚傳統金融如何整合其他數位資產或衍生性商品以及它們對去中心化的可能產生的副作用。

While the US capital market will be more exposed to ETH, leading to more permanent (structured) winds, it is unclear how traditional finance integrates other digital or derivative goods and their possible side effects on decentralisation.

1)傳統金融ETH與stETH

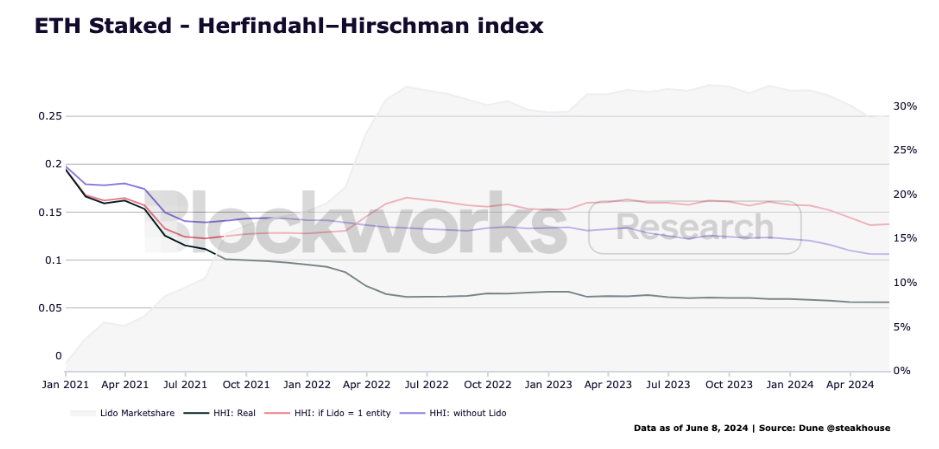

從哲學上講,我們認為LST是保持足夠去中心化、安全和高效能的驗證節點集的最佳方式。 Grandjean等人計算了以太坊的HHI指數(一種評估市場集中度和競爭力的指標),發現Lido已經改善了去中心化(如下圖中較低的HHI讀數所示)。

Philosophy, we think that LST is the best way to maintain enough central, safe, and efficient testing nodes. Grandjean et al., using the Taiyo HHI index (a guide for evaluating market concentration and competition), finds that Lido has improved decentralisation (as shown in the lower HHI readings below).

雖然將Lido視為一個實體會導致較高的HHI(即網絡較不去中心化),但我們不認為這種對Lido的描述準確地反映了Lido在市場中的存在,因為該協議不由一個組織或實體管理或控制,而驗證節點集由各種獨立的分開實體組成。雖然大型LSPs(質押服務提供者)存在風險,但實施適當的治理機制和協議監督,例如雙重治理,應該可以減輕其嚴重性。此外,預計DVT的加入將進一步分散營運商集合。

While treating Lido as an entity that leads to a higher HHI (i.e. the Internet is less central), we do not believe that this description of Lido accurately reflects the presence of Lido in the market, because the agreement is not managed or controlled by an organization or entity, and the test nodes are composed of separate entities. While there are risks in large LSPs, there are appropriate governance mechanisms and regulatory oversight, such as double governance, which should reduce its severity.

話雖如此,考慮到質押ETH的經濟激勵,或者說持有原生ETH會被稀釋的情況下,傳統金融最終提供質押ETH產品是有可能的。一些可能的(純粹是)假設的結果包括:

In spite of this, it is possible for traditional finance to eventually provide the ETH product, taking into account the economic incentives to hold the ETH, or where the possession of the original ETH would be diluted. Some of the possible (purely) outcomes include:

傳統金融明確採用stETH及其所有的好處

Traditional finance explicitly uses stETH and all its benefits.

傳統金融與Coinbase或其他大型機構質押服務提供者密切合作,建立這個框架,其中cbETH或tradfiETH成為傳統金融的正式質押ETH產品

Traditional finance works closely with Coinbase or other large institutional providers to establish this framework, where cbETH or tradfiETH becomes the official pledge of ETH products in traditional finance

傳統金融發展自己的做法,投資專有的節點運營,託管自己的質押ETH,並發行tradfiETH產品。

Traditional finance develops its own practices, invests in specialized nodes, holds its own ETH and issues tradfiETH products.

「雖然對於BTC [和ETH]來說這一切都很好,但未來的發展有些未知。」- DegenSpartan

"It's all good for the BTC [and the ETH], but there's a little bit of an unknown development." - DegenSpartan.

我們相信,並有證據表明,從假設的情景來看,(1)是網絡的更好解決方案,因為無論如何,如果質押ETH朝著傳統金融ETH的趨勢發展,鏈上的質押風險會趨向中心化。因此,在高度資本化的現有參與者開發中心化的質押產品的情況下,只要Lido保持足夠的去中心化,stETH和DAO都是維持以太坊整體一致性的關鍵因素,因為DAO管理stETH的委託,並且間接影響網路的效能、安全性和去中心化。

We believe, and there is evidence to suggest, that (1) is a better solution for the Internet, given that, in any event, the risk of chain-based pledge of ETH is centralized if the hostage is moving towards the traditional financial ETH. Thus, in the case of the centrally developed products of highly capitalized present participants, as long as Lido remains sufficiently central, stETH and DAO are key factors in maintaining overall euphoric coherence, given the DAO’s mandate to manage the ETH and, in turn, influence the effectiveness, security and decentralization of the Internet.

2)風險

波動性和流動性:當ETH的波動性激增時,投資者更願意在公開市場上出售stETH,而不是等待提取隊列。在高波動期間,如果沒有足夠的流動性,高銷售量可能導致stETH的價格偏離其與ETH的1:1價格錨定,這帶來了隨後的風險,直到市場條件恢復。

Wave and fluidity: When ETH surges, investors prefer to sell stETH on the open market instead of waiting for extraction. During high wave activity, if there is not enough fluidity, high sales may result in stETH's price being set at 1:1 below the ETH, which poses a subsequent risk until market conditions are restored.

循環風險:一種常見的賺取獎勵的方法(例如參與空投或流動性挖礦激勵),用戶採取槓桿頭寸,借出stETH,借入ETH,購買stETH,借出額外的stETH,並重複循環,直到他們完全槓桿化到最大容量。在波動時期,循環者面臨被清算的風險,可能觸發與波動性和流動性相關的放大風險。

Environmental risk: A common way of earning rewards (e.g. by participating in airdrops or mobile mining incentives), users take a stick position, borrow a stETH, borrow an ETH, borrow an extra stETH, and repeat the loop until they reach maximum capacity. During a wave, the looper faces a liquidation risk that could trigger a magnifying risk associated with wave and fluidity.

協議與治理:與LSP佔據重要市場份額相關的風險。 stETH委託的協議由DAO管理。雖然DAO正在朝著雙重治理邁出步伐,這將減少這些風險,但如果stETH佔據了質押ETH的大部分份額,那麼對ETH份額集中化到LDO治理的擔憂是有理由的。

Agreement and governance: The risks associated with the LSP’s occupation of important markets. The agreement commissioned by the stETH is administered by DAO. While DAO is moving toward double governance, this will reduce these risks, but if stETH is holding a large share of the ETH, there is a reason to worry about centralizing the ETH to LDO governance.

智能合約:Lido協定由一系列智能合約執行。這包括存款、提款、委託質押、懲罰和密鑰管理。這些系統中存在著與智慧合約相關的未預料的錯誤或惡意升級。

Smart contract: Lido's agreement is executed by a series of smart contracts. This includes deposits, withdrawals, bailing, penalties, and key management. There are unexpected errors or malignant upgrades in these systems associated with intellectual agreement.

競爭對手:LST市場龐大,並且有更多的重新質押協議進入競爭領域。傳統金融也有能力開發自己的質押產品,鑑於目前的市場結構,這可能對某些投資者更具可近性。

Competition: The LST market is huge, and there are more re-privileged agreements to enter the competition. Traditional finance also has the ability to develop its own collateral, which is more relevant to some investors than the current market structure.

監管:儘管現貨ETH ETF的批准可能使質押服務提供者在平均水平上更安全,但對質押ETH仍將進行監管審查。相關的法律討論包括(但不限於)質押服務提供者的角色、根據豪伊測試的「管理」和「行政」之間的區別,以及LSPs是否是「發行人」(根據Reve測試)。

Monitoring: While the approval of the current ETH ETF may make the delivery service provider safer on average, the custody of the ETH will continue to be subject to supervisory scrutiny. The related legal discussion includes (but is not limited to) the role of the delivery service provider, the difference between "management" and "administration" according to the Howie test, and whether the LSPs are "issuers" (according to Reve test).

以現今的標準,stETH可以說是獲得質押ETH參與度最好的產品。它是鏈上最流動的LST,是DeFi中最廣泛使用的抵押品形式,而這些市場結構正在迅速擴展到鏈下,這一點已透過交易平台的交易量成長(尤其是ByBit和OKX)得到證明。

By today’s standards, stETH can be described as the best product to secure ETH’s involvement. It is the most fluid LST on the chain, the most widely used form of collateral in DeFi, and these market structures are rapidly spreading under the chain, as evidenced by the growth of trading platforms (especially ByBit and OKX).

雖然持有stETH存在風險,但這些強大的市場結構很可能會繼續存在並可能在stETH的屬性、Lido的協議、對以太坊整體一致性的日益增長的需求以及即將到來的催化劑的推動下進一步擴大。路線圖上的這些催化劑包括分散式驗證者技術(DVT)、雙重治理、支援預先確認並分配額外資源用於重新質押stETH,以及一種改進的治理結構,將有助於以太坊研究。更重要的是,如果傳統金融開發質押ETH產品,stETH和LidoDAO將在以太坊更廣泛範圍內發揮越來越重要的作用。

Despite the risks associated with holding stETH, these powerful market structures are likely to continue to exist and may be associated with stETH attributes, Lido’s agreement, the growing demand for Ether’s overall consistency, and the impending push for catalytic agents. These catalysts on the road map include decentralized tester techniques (DVT), double governance, support to pre-reconfirmation and allocation of extra resources for the re-prising of stETH, and an improved governance structure, will be instrumental in the development of ETH products.

注册有任何问题请添加 微信:MVIP619 拉你进入群

打开微信扫一扫

添加客服

进入交流群

发表评论