-

比特币ETF为许多新投资者提供了将比特币纳入其投资组合的机会。相比之下,以太坊ETF的影响尚不明朗。

BitcoinETF provides many new investors with the opportunity to include bitcoin in their portfolio. By contrast, the impact of the Tepan ETF is unclear.

当贝莱德提交比特币ETF申请时,我在比特币价格为25,000美元时看涨。从那时起,比特币价格上涨了2.6倍,而以太坊上涨了2.1倍。从周期底部开始,比特币和以太坊的回报率均为4.0倍。那么,以太坊ETF能带来多少上行空间呢?我认为,如果以太坊不能找到提升经济效益的有力途径,其上行空间有限。

When Belet submitted the Bitcoin ETF application, I saw it rise at a price of $25,000. Since then, Bitcoin has increased by 2.6 times, while it has risen by 2.1 times as much as in the Taiku. From the bottom of the cycle, Bitcoin and Etae have a rate of return of 4.0 times.

资金流动分析

Analysis of Financial Flows

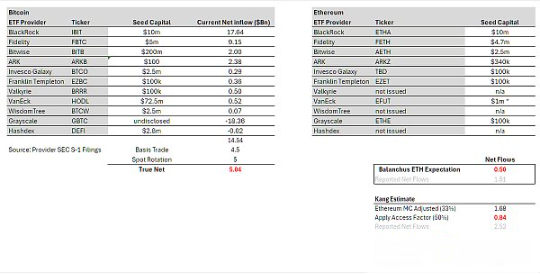

总体来看,比特币ETF积累了500亿美元的资产管理规模,这是一个令人印象深刻的数字。然而,如果将现有的GBTC资产管理规模和轮换排除在外,自推出以来的净流入仅为145亿美元。这些并非真正的流入,因为需要考虑许多中性资金流,如基差交易(卖出期货,买入现货ETF)和现货轮换。根据CME的数据和对ETF持有者的分析,我估计大约有45亿美元的净流入可以归因于基差交易。ETF专家认为,如BlockOne等大型持有者还将现货比特币转换为ETF,约为50亿美元。扣除这些流量后,我们得出比特币ETF的真实净买入为50亿美元。

Overall, Bitcoin ETF has accumulated $50 billion in asset management, which is an impressive figure. However, if the size and rotation of the existing GBTC asset management were excluded, the net inflow has been only $14.5 billion since its introduction. These are not real inflows, because there are many neutral financial flows that need to be considered, such as base transactions (sale of futures, purchase of spot ETFs) and spot rotations. On the basis of CME data and analysis of ETF holders, I estimate that the net inflow of approximately $4.5 billion can be attributed to base transactions.

以太坊的情况

从这里我们可以简单地推算出以太坊的情况。分析师Eric Balchunas估计,以太坊的流入可能是比特币的10%。这意味着在6个月内真实净买入为5亿美元,报告的净流入为15亿美元。尽管Balchunas对批准几率的估计有误,但我认为他对以太坊ETF的兴趣缺乏和悲观态度具有信息性,反映了传统金融对其的广泛兴趣。

This means a real net buy-in of $500 million in six months, and a net transfer of $1.5 billion in the report. Despite Balchunas’ misapproach of approval options, I think he is informative about his lack of interest and pessimism in ETF, reflecting the widespread interest in traditional finance.

个人预测

我的基准是15%。从比特币的50亿美元真实净买入开始,调整以太坊的市值为比特币的33%和一个0.5的访问因子,我们得出真实净买入为8.4亿美元,报告的净流入为25.2亿美元。有合理的观点认为,与GBTC相比,ETHE的溢价较少,所以我将乐观情景设定为15亿美元真实净买入和45亿美元报告的净流入。这大约是比特币流入的30%。

My benchmark is 15%. Starting with a real net buy-in of $5 billion in bitcoin, adjusting the market value of the taupulega to 33% of bitcoin and a 0.5 visit factor, we came up with a real net buy-in of $840 million and a reported net inflow of $2.52 billion. There is a reasonable argument that the ETHE premium is lower than that of the GBTC, so I set my optimism at a real net buy-in of $1.5 billion and a reported net inflow of $4.5 billion. This is about 30% of the inflow of bitcoin.

在任何情况下,真实净买入远低于ETF前的衍生品流动,这些衍生品流动总计28亿美元,并且不包括现货提前布局。这意味着ETF的影响已被价格充分反映。

In any case, real net purchases are much lower than the pre-ETF derivative flows, which total $2.8 billion, and do not include pre-positioning of the spot. This means that the ETF’s impact has been adequately reflected in prices.

比特币与以太坊ETF的市场反应

bitcoin and Etheria ETF's market response

50亿美元是如何将比特币从40,000美元推高到65,000美元的?简短的回答是,它并没有。现货市场上还有许多其他买家。比特币已成为全球认可的关键投资资产,拥有许多结构性累积者,如Michael Saylor、Tether、家族办公室、高净值个人等。以太坊也有一些结构性累积者,但我认为其数量远低于比特币。

How does the $5 billion push bitcoin from $40,000 to $65,000? The short answer is that it does not. There are many other buyers in the spot market. Bitcoin has become a globally recognized key investment asset with many structural accumulations, such as Michael Saylor, Tether, family offices, and high net worth individuals.

比特币在ETF存在之前已经达到过69,000美元/1.2万亿美元以上的市值。市场参与者/机构拥有大量现货加密货币。Coinbase托管了1930亿美元,其中1000亿美元来自其机构计划。2021年,Bitgo报告托管了600亿美元,Binance托管了超过1000亿美元。ETF推出后6个月,托管了比特币总供应量的4%,这很重要,但只是需求方程的一部分。

Bitcoin had a market value of over $69,000/$1.2 trillion before the ETF existed. Market participants/institutions had a large amount of real-time encrypted currency. Coinbase hosted $193 billion, of which $100 billion came from its institutional plan. In 2021, Bitgo reported that it hosted $60 billion, and Binance held over $100 billion. Six months after ETF was launched, it hosted 4 per cent of the total supply of Bitcoin, which is important, but only part of the demand equation.

以太坊ETF的定位与前景

with the position and perspective of the Taiyo ETF

以太坊ETF的定位非常不同。以太坊在推出前的价格是低点的4倍,而比特币为2.75倍。加密货币交易所的未平仓合约增加了21亿美元,使其接近历史最高水平。市场是(半)有效的。许多加密货币参与者看到比特币ETF的成功,期望以太坊也能获得同样的结果,并据此进行布局。

The location of the ETF is very different. The price of the ETF was four times lower before it was launched, compared to 2.75 times that of Bitcoin. The unsettled contracts of the encrypted currency exchange increased by $2.1 billion, bringing them close to the highest level ever. The market is (half) effective. Many of the encoded currency participants see the success of the ETF, and expect that the same results will be achieved by the ETF, which will be configured accordingly.

我个人认为,加密货币参与者的预期被高估了,与传统金融配置者的真实偏好脱节。那些深耕加密领域的人对以太坊有相对较高的认同感和购买意愿。然而,实际上,对于许多非加密货币本土资本的大型群体而言,以太坊作为关键投资组合配置的认同度要低得多。

Personally, it seems to me that the expectations of participants in cryptographic money are overestimated, out of line with the true preferences of traditional financial configurations. Those in the field of deep-deep encryption have a relatively high sense of identity and willingness to buy. In practice, however, for large groups of non-encrypted local capital, the profile of Taipan as a key portfolio is much lower.

结论

向传统金融推销以太坊最常见的理由之一是将其视为“科技资产”。全球计算机、Web3应用商店、去中心化金融结算层等。这是一个不错的推销点,在前几个周期中我也曾相信过。但当你看实际数字时,这却很难令人信服。

One of the most common reasons for traditional financial marketing is to think of it as a “scientific asset.” Global computers, Web3 applications, decentralized financial clearing houses, etc. This is a good marketing point that I have believed in in previous cycles. But when you look at actual numbers, it is hard to believe.

在上一个周期中,你可以指出费用的增长率,并指出DeFi和NFT会产生更多费用、现金流等,从而使其成为一个像科技股一样的科技投资。但在这个周期中,费用的量化却适得其反。大多数图表显示增长持平或负增长。以太坊是一个现金机器,但在1.5亿美元30天年化收入、300倍市销率、通胀后的负收益/市盈率下,分析师如何向家族办公室或宏观基金老板解释这个价格?

In the previous cycle, you could point to the growth rate of costs, and point out that DeFi and NFT would generate additional costs, cash flows, and so on, making it an investment in technology like a science and technology unit. But in this cycle, the quantification of costs is counterproductive.

以太坊不会归零,但在某个价格下,它将被视为有价值的资产。当比特币在未来上涨时,它会在一定程度上被带动上涨。在ETF推出前,我预计以太坊的交易价格在3,000美元至3,800美元之间。ETF推出后,我的预期是2,400美元至3,000美元。然而,如果比特币在2024年底/2025年第一季度涨到100,000美元,那么这可能会带动以太坊达到历史新高,但以太坊/比特币的比率会更低。从长期来看,仍有许多发展值得期待,你必须相信Blackrock/Fink正在做大量工作,以在区块链上建立一些金融轨道并令更多资产代币化。这将为以太坊带来多少价值以及在何种时间线上尚不确定。

At the end of 2024 and the first quarter of 2025, however, it may lead to an historic high, but at a lower rate. In the long run, there are still a lot of developments to be expected, and you must believe that Blackrock/Fink is doing a lot of work to build some of the financial tracks on the regional chains and to make more assets monetized. This will be uncertain as to how much value will come from Taiku and what time frame.

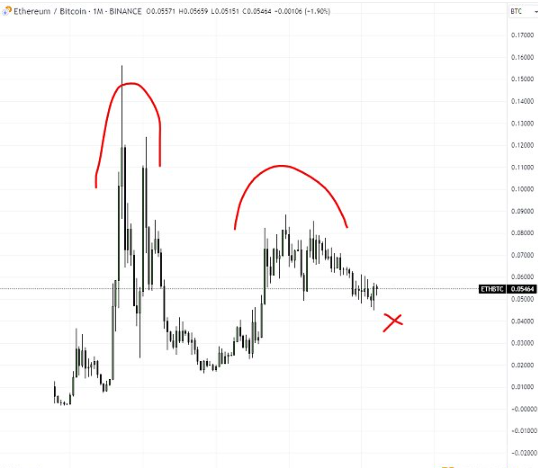

未来一年以太坊/比特币的比率将继续下跌,范围在0.035至0.06之间。尽管样本量很小,但我们看到以太坊/比特币在每个周期都创下更低的高点,因此这不应令人意外。

In the coming year, the rate will continue to fall between 0.035 and 0.06. Although the sample size is small, it should not be surprising that we see that the rate is lower in every cycle.

?

?注册有任何问题请添加 微信:MVIP619 拉你进入群

打开微信扫一扫

添加客服

进入交流群

发表评论